Asia's Race to 2030 Has Begun: What Does It Mean for India?

BGV team went to Ecosperity in 2026And, came back with this series.

Every year, Ecosperity has a way of reordering your priorities. This year was no different - except the signal was louder than usual.

Within the first few discussions, a theme had emerged - not because anyone announced it, but because every serious conversation kept arriving at the same place. AI, energy, and climate transition are colliding at scale. The centre of gravity has shifted. Climate is no longer primarily a conversation about ESG targets or distant net-zero pathways. It is increasingly a conversation about infrastructure - grids, cooling systems, power generation, -and the stress that AI is placing on all of them simultaneously.

BGV team went to Ecosperity in 2026

And, came back with this series.

Every year, Ecosperity has a way of reordering your priorities. This year was no different - except the signal was louder than usual.

Within the first few discussions, a theme had emerged - not because anyone announced it, but because every serious conversation kept arriving at the same place. AI, energy, and climate transition are colliding at scale. The centre of gravity has shifted. Climate is no longer primarily a conversation about ESG targets or distant net-zero pathways. It is increasingly a conversation about infrastructure - grids, cooling systems, power generation, -and the stress that AI is placing on all of them simultaneously.

Which is what brought us back to India.

At BlueGreen Ventures, we have long believed that India's most significant climate opportunities would emerge not from narrative, but from real system stress. This year at Ecosperity, that belief found its clearest validation yet - and one report in particular crystallised it.

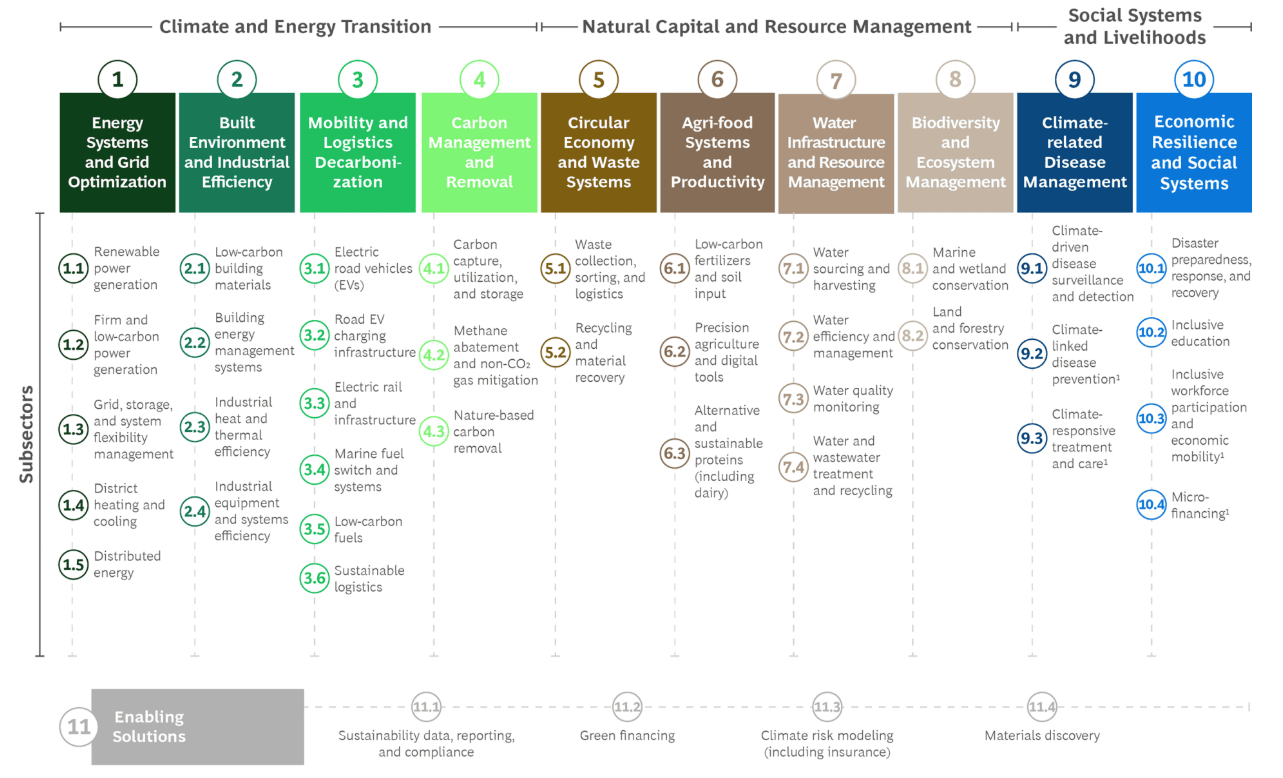

Released at Ecosperity Week itself, the BCG and Temasek report - The Private Capital Opportunity in AI-Enabled Climate and Sustainability Sectors does something most climate investment research doesn't: it connects the AI boom directly to sustainability returns, and puts a number on it. Their headline finding: deploying current AI capabilities across climate and sustainability sectors could generate approximately $600 billion in annual global value by 2028, across more than 40 subsectors.

Released at Ecosperity Week itself, the BCG and Temasek report - The Private Capital Opportunity in AI-Enabled Climate and Sustainability Sectors does something most climate investment research doesn't: it connects the AI boom directly to sustainability returns, and puts a number on it. Their headline finding: deploying current AI capabilities across climate and sustainability sectors could generate approximately $600 billion in annual global value by 2028, across more than 40 subsectors.

Critically, BCG and Temasek only count subsectors where a clear chain exists from AI capability → commercial value → sustainability outcome. It is not a list of everything AI touches. It is a map of where efficiency gains and climate outcomes are structurally linked. One of their five priority subsectors: grid, storage, and system flexibility.

That is exactly where this piece begins.

Part 1: The Grid is Breaking – And That's the Opportunity

For most of the last century, grid planners had a job that was difficult but manageable. They could model demand. Peak load came in summer - in India, reliably in June, with predictable festival surges around Diwali and exam season. Factories ran on predictable shifts. You built for roughly 30% headroom above peak demand, and you slept at night.That world ended around 2022.

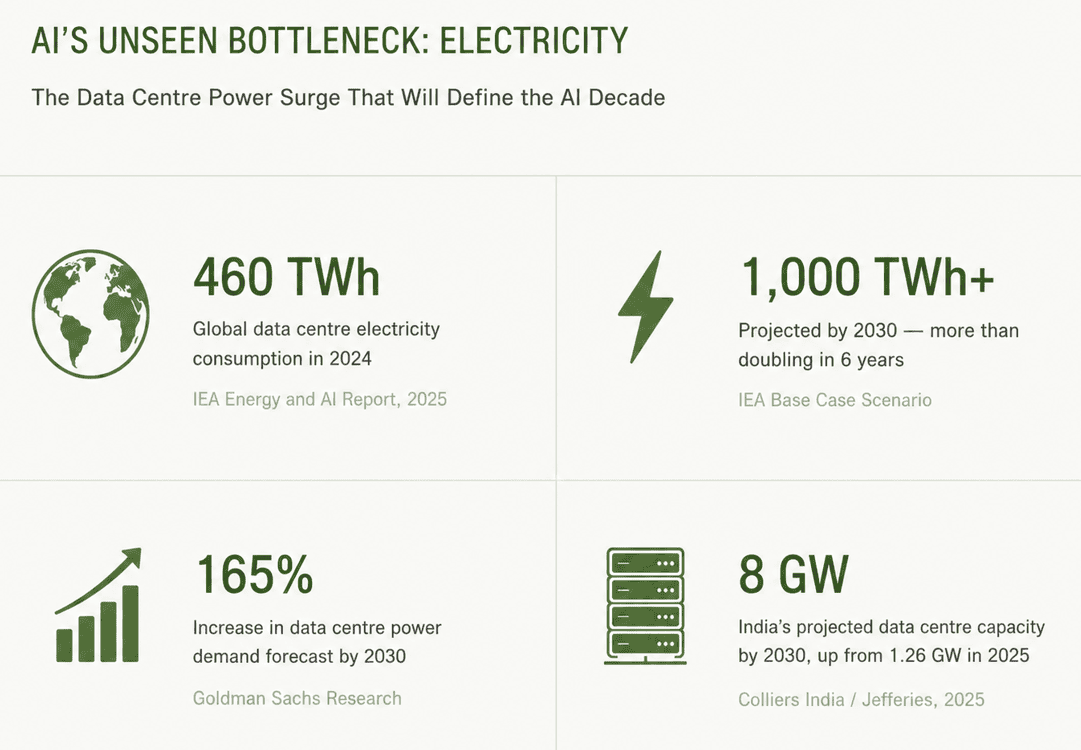

AI has made it worse every year since. Every time a user types a query into an AI model, they trigger a compute process that consumes roughly 10 times more electricity than a traditional Google search (IEA, Energy and AI, 2025). Multiply that by billions of daily queries across ChatGPT, Gemini, Grok, and dozens of Indian-built models launching under the IndiaAI Mission - and you have an invisible, unpredictable, massive new electricity consumer that has no off-season, no festival calendar, and no regard for grid stability.

That world ended around 2022.

AI has made it worse every year since. Every time a user types a query into an AI model, they trigger a compute process that consumes roughly 10 times more electricity than a traditional Google search (IEA, Energy and AI, 2025). Multiply that by billions of daily queries across ChatGPT, Gemini, Grok, and dozens of Indian-built models launching under the IndiaAI Mission - and you have an invisible, unpredictable, massive new electricity consumer that has no off-season, no festival calendar, and no regard for grid stability.

India's data centre story is particularly striking. Capacity grew from 0.3 GW in 2018 to 1.26 GW in April 2025 and is projected to reach 8 GW by 2030. The sector attracted $95 billion in investment between 2019 and 2025. Reliance is building a 1.5 GW campus. L&T is partnering with NVIDIA on a sovereign AI factory in Chennai. AWS, Google, and Microsoft are all expanding cloud regions in India. The shovels are already in the ground.

The brutal arithmetic: In 2025, Indian data centres already consumed 0.5% of the country's total electricity and approximately 150 billion litres of water - both figures projected to more than double by 2030 (MarketsandMarkets, February 2026). This is happening in a country where the grid was already stressed before AI entered the picture.

More demand means more coal. The numbers are uncomfortable.

India's renewable story is real and worth celebrating. By January 2026, non-fossil capacity crossed 52% of total installed capacity. Renewables covered all incremental demand growth in 2025. But here is what the Ecosperity speakers were quietly circling: installed capacity and actual generation are two very different numbers.

Solar only generates during the day. Wind is intermittent. When demand spikes at 3:30 PM on a 43-degree June afternoon in Delhi, the grid reaches for whatever is dispatchable right now. That dispatchable baseload, right now, is still coal. Coal fuels over 74% of India's actual power generation and contributes 55% of the national energy mix (Ministry of Coal / PIB India, March 2025). India became the first country ever to produce over 1 billion tonnes of coal in a single financial year in FY 2024-25 - and the government plans to add 100 GW of new coal capacity over the next seven years (CREA, January 2026).

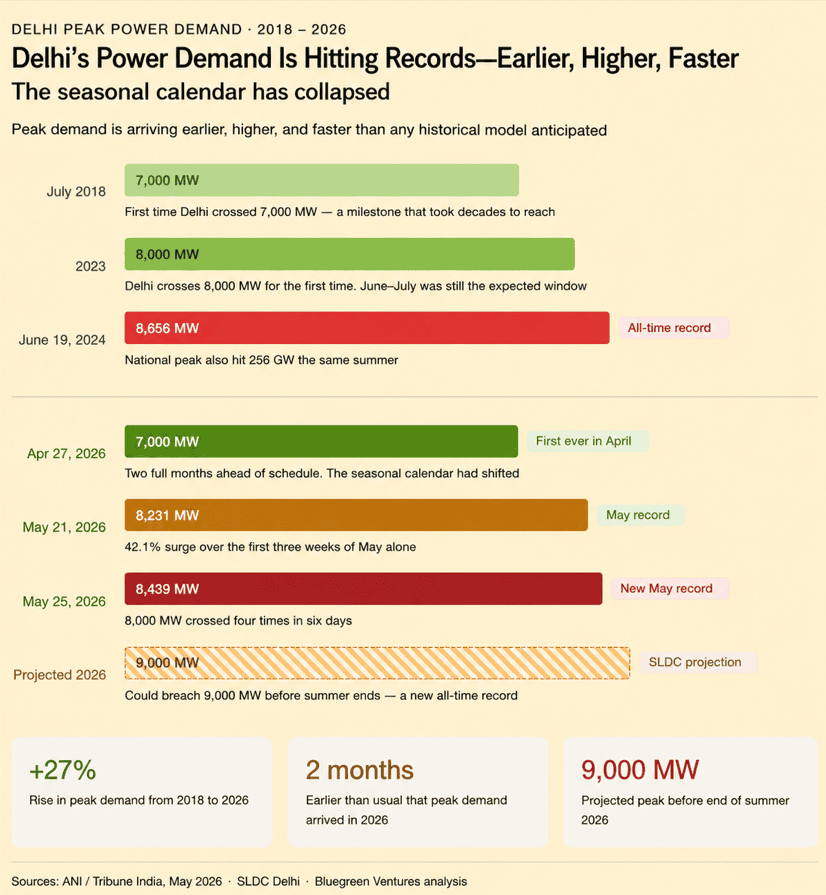

GROUND TRUTH - DELHI, SUMMER 2026

Delhi Is the Most Vivid Data Point We Have

You want to understand the grid stress problem? Don't look at models. Look at Delhi this summer. Delhi is becoming a real-time case study of grid stress. Peak power demand is arriving earlier and reaching higher levels than historical patterns suggest.

Between May 1–25, 2026, demand exceeded 2025 levels on 80% of days and 2024 levels on 72% of days, while India hit a record peak demand of 256 GW in April - months ahead of the traditional summer peak.

Where we are paying close attention

We started Bluegreen because we believe India's climate-tech opportunity is still dramatically underinvested at the early stage. The macro above confirms this isn't a theme story - it is an infrastructure emergency with a venture-fundable solution set. And infrastructure emergencies, historically, are where the most durable companies get built.

Grid intelligence - the layer that makes everything else possible

Before India can transition its energy mix, before it can absorb 500 GW of renewables, before it can power the data centres it is building at speed - it needs a grid that can think in real time. Right now, it doesn't have one.

India's grid was engineered for a centralised, coal-dominated, highly predictable world. Fixed generation sources. Known demand curves. Seasonal peaks that planners had decades to prepare for. That architecture is now being asked to handle something it was never designed for: variable renewable generation on one side, and AI-driven, non-seasonal, non-predictable demand spikes on the other.

The gap between what the grid can do and what it needs to do is where we see the clearest early-stage opportunity right now.

The Opportunity: Here is the paradox few said out loud at Ecosperity - the same technology stressing India's grid is also the most powerful tool to stabilise it. AI created the unpredictability problem. AI-driven grid intelligence is how we solve it.

For the first time, it is possible to forecast demand variability in real time, anticipating data centre load spikes, rooftop solar drops, and unplanned industrial draws before they hit. Demand-response platforms can turn large consumers into active grid participants, curtailing load in milliseconds when the grid needs relief. Grid-forming battery systems, guided by AI dispatch logic, can provide the frequency stability that coal plants once provided -without a single tonne of fuel. Distribution automation removes the human bottleneck from load management. And smart meter analytics - across 250 million endpoints - creates an intelligence layer India's grid has never had.

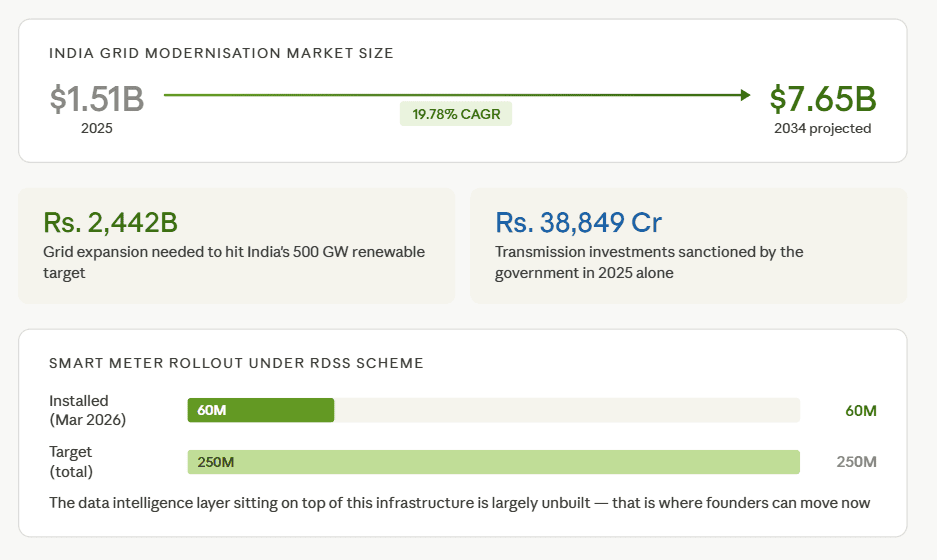

The grid doesn't need to be rebuilt. It needs to be made intelligent. The Numbers:- India's grid modernisation market was valued at $1.51 billion in 2025and is projected to reach $7.65 billion by 2034, growing at a 19.78% CAGR (IMARC Group, 2026).

- To achieve its 500 GW renewable energy target, India requires approximately ₹2,442 billion in grid expansion investments (IFRI, 2026).

- In 2025 alone, the government sanctioned ₹38,849 crore for transmission infrastructure investments (PV Magazine India, 2026).

- As of March 2026, 60 million smart meters have been installed under the RDSS scheme, nearly doubling the previous year's additions.

- The government's target is to deploy 250 million smart meters nationwide.

- Despite rapid infrastructure deployment, the data and software layer needed to fully leverage this grid infrastructure remains largely underbuilt, creating significant opportunities for innovation.

This is not a market that is years away. The regulatory mandate is live. The hardware rollout is accelerating. The demand signal from AI is already hitting the grid this summer. The founders who move now are building into an infrastructure gap that is only going to widen.

Grid intelligence - the layer that makes everything else possible

Before India can transition its energy mix, before it can absorb 500 GW of renewables, before it can power the data centres it is building at speed - it needs a grid that can think in real time. Right now, it doesn't have one.

India's grid was engineered for a centralised, coal-dominated, highly predictable world. Fixed generation sources. Known demand curves. Seasonal peaks that planners had decades to prepare for. That architecture is now being asked to handle something it was never designed for: variable renewable generation on one side, and AI-driven, non-seasonal, non-predictable demand spikes on the other.

The gap between what the grid can do and what it needs to do is where we see the clearest early-stage opportunity right now.

The Opportunity: Here is the paradox few said out loud at Ecosperity - the same technology stressing India's grid is also the most powerful tool to stabilise it. AI created the unpredictability problem. AI-driven grid intelligence is how we solve it.

For the first time, it is possible to forecast demand variability in real time, anticipating data centre load spikes, rooftop solar drops, and unplanned industrial draws before they hit. Demand-response platforms can turn large consumers into active grid participants, curtailing load in milliseconds when the grid needs relief. Grid-forming battery systems, guided by AI dispatch logic, can provide the frequency stability that coal plants once provided -without a single tonne of fuel. Distribution automation removes the human bottleneck from load management. And smart meter analytics - across 250 million endpoints - creates an intelligence layer India's grid has never had.

The grid doesn't need to be rebuilt. It needs to be made intelligent.

The Numbers:

- India's grid modernisation market was valued at $1.51 billion in 2025and is projected to reach $7.65 billion by 2034, growing at a 19.78% CAGR (IMARC Group, 2026).

- To achieve its 500 GW renewable energy target, India requires approximately ₹2,442 billion in grid expansion investments (IFRI, 2026).

- In 2025 alone, the government sanctioned ₹38,849 crore for transmission infrastructure investments (PV Magazine India, 2026).

- As of March 2026, 60 million smart meters have been installed under the RDSS scheme, nearly doubling the previous year's additions.

- The government's target is to deploy 250 million smart meters nationwide.

- Despite rapid infrastructure deployment, the data and software layer needed to fully leverage this grid infrastructure remains largely underbuilt, creating significant opportunities for innovation.

This is not a market that is years away. The regulatory mandate is live. The hardware rollout is accelerating. The demand signal from AI is already hitting the grid this summer. The founders who move now are building into an infrastructure gap that is only going to widen.

Our Framing

We are not here to solve the grid. We are here to fund the people who will.

One thing the Ecosperity session made clear: the people complaining loudest about the energy transition gap are often the least positioned to close it. Multilateral banks debate blended finance structures. Governments release targets. The discourse is rich. The execution remains thin.

At Bluegreen, we have a specific, focused role: find the founders who see this infrastructure gap as a product opportunity, back them early, and help them scale into one of the largest infrastructure build-outs Asia will see this decade.

The climate case and the investment case are not in tension here. They are the same case. Every MW of grid intelligence deployed reduces the chance of a cascading blackout in a city of 32 million people. Every smart meter that goes live adds another data point to an intelligence layer that India desperately needs. Every demand-response platform that scales makes the grid more resilient to the next heatwave, the next AI demand spike, the next moment when the old predictability simply isn't there anymore.

This is only the beginning of what we saw at Ecosperity.

In Part 2, we dive into why India's carbon markets are live and compliance pressure on steel, cement, aluminium and fertiliser is real, but the infrastructure to actually run these markets barely exists. We map exactly where founders can build it.

If you are building in any of these spaces - reach out. We are paying attention.

We are not here to solve the grid. We are here to fund the people who will.

One thing the Ecosperity session made clear: the people complaining loudest about the energy transition gap are often the least positioned to close it. Multilateral banks debate blended finance structures. Governments release targets. The discourse is rich. The execution remains thin.

At Bluegreen, we have a specific, focused role: find the founders who see this infrastructure gap as a product opportunity, back them early, and help them scale into one of the largest infrastructure build-outs Asia will see this decade.

The climate case and the investment case are not in tension here. They are the same case. Every MW of grid intelligence deployed reduces the chance of a cascading blackout in a city of 32 million people. Every smart meter that goes live adds another data point to an intelligence layer that India desperately needs. Every demand-response platform that scales makes the grid more resilient to the next heatwave, the next AI demand spike, the next moment when the old predictability simply isn't there anymore.

This is only the beginning of what we saw at Ecosperity.

In Part 2, we dive into why India's carbon markets are live and compliance pressure on steel, cement, aluminium and fertiliser is real, but the infrastructure to actually run these markets barely exists. We map exactly where founders can build it.

If you are building in any of these spaces - reach out. We are paying attention.

Part 2: Carbon Markets: India’s Next Infrastructure Play

India has spent the last three years quietly building the regulatory plumbing for a multi-billion dollar carbon market - and the startup ecosystem still hasn't priced it in. The Carbon Credit Trading Scheme (CCTS) is one of the most consequential policy developments, yet one of the least understood by founders and investors.

In Part 2 of this series, we go one layer deeper than the grid intelligence market we talked about in Part 1: here's what actually happened, how fast it moved, and why it matters for anyone building in this space. Here is what has happened, and fast:

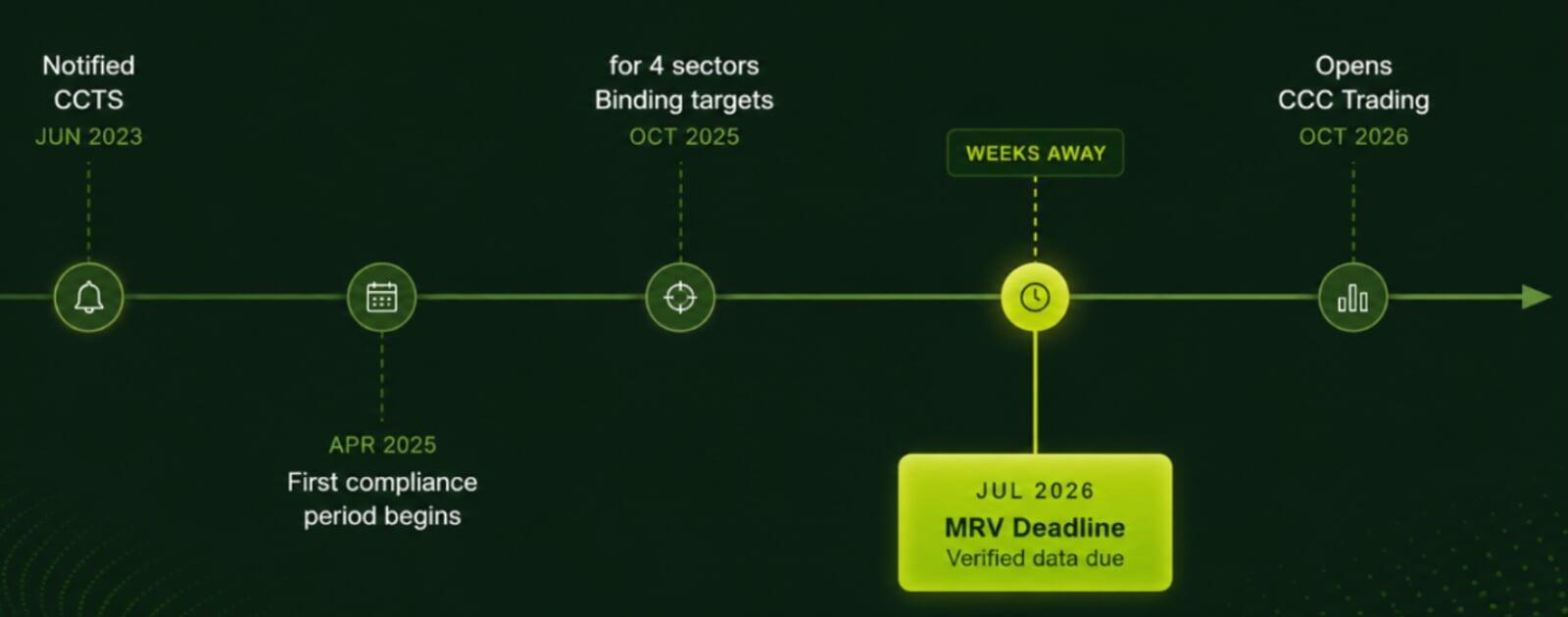

- June 2023: CCTS officially notified under the Energy Conservation (Amendment) Act, 2022.

- April 2025: First compliance period begins, FY 2025-26 emission reduction targets come into effect for all notified sectors.

- October 2025: Binding emission intensity targets notified for the first four sectors: Aluminium, Cement, Chlor-alkali, and Pulp & Paper

- January 2026: Additional sectors brought under the scheme: Petroleum Refining, Petrochemicals, and Textiles

- April 2026: Obligated entities required to submit action plans to the Bureau of Energy Efficiency (BEE) outlining how targets will be achieved.

- July 2026: Monitoring, Reporting, and Verification (MRV) reporting deadline:

- Facilities must submit verified FY 2025-26 emissions data.

- Verification must be conducted by a BEE-accredited third-party agency.

- October 2026: Carbon Credit Certificate (CCC) trading opens on the designated power exchange, with the first trades expected to commence

- Facilities must submit verified FY 2025-26 emissions data.

- Verification must be conducted by a BEE-accredited third-party agency.

As of FY 2025-26, approximately 490 entities across seven sectors now have legally binding GHG emission intensity targets, with the remaining two sectors (iron & steel, fertilisers) to follow. Once fully operational, the CCTS will cover around 740 entities and over 700 million tonnes of CO2 emission - placing India among the world's largest emissions trading systems.

The financial stakes are not abstract. Under the CCTS, non-compliance incurs an "environmental compensation" equal to twice the average carbon credit price. Entities that outperform their targets earn Carbon Credit Certificates (CCCs) they can sell. Entities that fall short must buy CCCs or pay the penalty. This is not a soft ESG commitment. This is a financial instrument with a hard deadline.

And the deadline is July 2026. But here is the problem nobody is solving yet

The compliance machinery is in place. The legal obligations are clear. The penalties are real.

India's compliance carbon market now has sectoral targets, regulatory obligations, and a clear path to trading. What remains underbuilt is the infrastructure required to make the system work at scale.

As EY India noted in March 2026, credit issuance under the compliance mechanism has yet to begin, highlighting ongoing gaps in MRV systems, data governance, and trading infrastructure.

This is where the opportunity lies. Every carbon market depends on trusted measurement, verification, compliance workflows, and market access. As India's carbon economy takes shape, the companies building these digital rails may become as valuable as the credits themselves.

The signal is already visible. Climate Change Response (CCR) expanded its India operations in 2026 to meet rising demand for emissions measurement and compliance capabilities- an early indicator of where market demand is heading.

The CBAM Pressure : A second clock is ticking

The domestic compliance deadline is urgent. But for India's industrial exporters, there is a second, equally urgent pressure: the EU's Carbon Border Adjustment Mechanism (CBAM), which entered its definitive phase on January 1, 2026.

CBAM applies a carbon levy on imports into the EU across six sectors: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. For India- one of the EU's key trading partners in precisely these sectors - the financial consequences are immediate.- India is expected to bear 18% of total CBAM costs globally - nearly double its share of EU import value.

- The Global Trade Research Initiative (GTRI) estimates Indian exporters may need to cut prices by 15–22% to absorb the CBAM tax burden.

- India estimates the levy could add an average tax burden of around 25% on affected exports to the EU.

- In the absence of verified product-level carbon data, EU authorities apply default - highest - emission values, sharply increasing CBAM costs even if actual emissions are lower.

That last point is the most important one for founders. The CBAM problem is fundamentally a data problem.

Indian exporters who cannot produce verified, product-level carbon intensity data will be assessed at default (worst-case) values - paying more than they need to, losing competitiveness to Chinese and Turkish competitors who can produce cleaner data faster.

India's steel carbon emission intensity of 2.4 tCO2 per tonne of steel significantly exceeds the global average of 1.85. (CSEP, August 2025). But even companies with better-than-average emissions lose if they can't prove it. The data infrastructure is the competitive advantage.

CBAM applies a carbon levy on imports into the EU across six sectors: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. For India- one of the EU's key trading partners in precisely these sectors - the financial consequences are immediate.

- India is expected to bear 18% of total CBAM costs globally - nearly double its share of EU import value.

- The Global Trade Research Initiative (GTRI) estimates Indian exporters may need to cut prices by 15–22% to absorb the CBAM tax burden.

- India estimates the levy could add an average tax burden of around 25% on affected exports to the EU.

- In the absence of verified product-level carbon data, EU authorities apply default - highest - emission values, sharply increasing CBAM costs even if actual emissions are lower.

That last point is the most important one for founders. The CBAM problem is fundamentally a data problem.

Indian exporters who cannot produce verified, product-level carbon intensity data will be assessed at default (worst-case) values - paying more than they need to, losing competitiveness to Chinese and Turkish competitors who can produce cleaner data faster.

India's steel carbon emission intensity of 2.4 tCO2 per tonne of steel significantly exceeds the global average of 1.85. (CSEP, August 2025). But even companies with better-than-average emissions lose if they can't prove it. The data infrastructure is the competitive advantage.

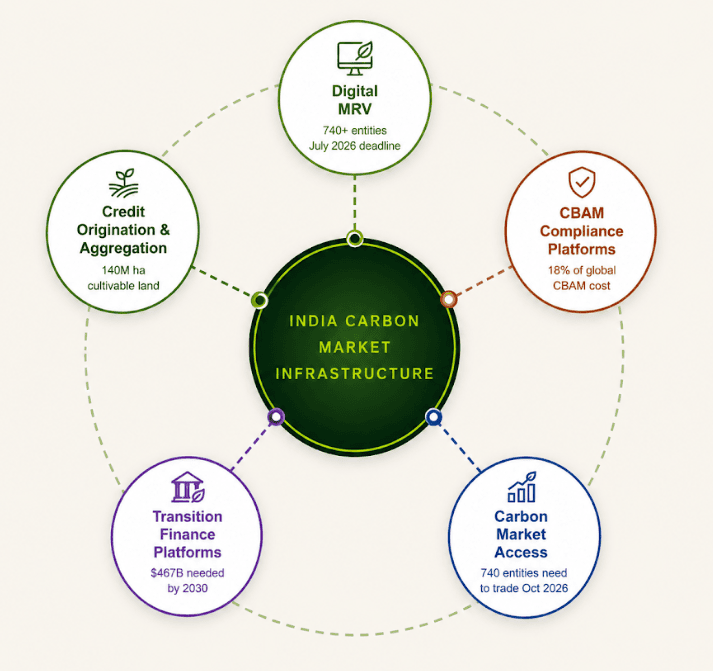

Where Founders Can Build : The Opportunity Map

The market infrastructure gap in India's carbon market is not one problem - it is five distinct, fundable problems. Here is how we are mapping them:

Layer 1 - Digital MRV Structure

The most immediate, most urgent opportunity.

- The opportunity: SaaS platforms that automate facility-level emissions data collection - integrating with energy meters, fuel invoices and production records to generate BEE-compliant MRV reports with audit trails. It can be thought of as compliance software for carbon - the equivalent of GST filing software when India's GST was first introduced.

- The numbers: BEE-accredited verification agencies already face bottleneck risk with 740+ entities competing for limited ACVA capacity before the July 2026 deadline. Digital platforms that reduce the cost and time of verification will capture a structurally large share of the compliance process.

Layer 2 - Carbon Credit Origination and Aggregation for MSMEs and Farmers

- The opportunity: Platforms that bring farmers and MSMEs into the voluntary carbon market through project origination, methodology compliance, credit aggregation, and buyer matching are the infrastructure we are currently lacking entirely. IIT Roorkee and the UP government's December 2025 farmer carbon credit programme is the working model; Varaha's Industrial Partners Programme shows it applied to industrial biomass partners. The bigger play is owning the technology layer, not the projects.

- The numbers: One UP pilot alone is generating Rs 5,000–8,000/hectare in supplementary farmer income - across a cultivable base of 140 million hectares, the upside is enormous. Varaha - backed by our GPs since 2022 - has removed 2 million+ tonnes of CO2 across 14 projects, holds offtake deals with Google, Microsoft, and Louis Dreyfus, and projects revenue growth from $4.76M to $22.15M in 2026 while staying profitable.

Layer 3 - CBAM Compliance Data Platforms for Exporters

- The opportunity: Product carbon footprint (PCF) platforms that help Indian steel, aluminium, and cement manufacturers generate verified, EU-recognised carbon intensity data for every shipment entering the EU from January 2026 - without verified data, exporters face the EU's highest default emission values, sharply raising CBAM costs.

- A secondary opportunity sits in Mutual Recognition Agreement infrastructure: technology that helps Indian certifying bodies win EU recognition so Indian-verified data is accepted without re-verification - government-facing, but a founder-buildable technical layer.

- The numbers: India's steel and aluminium exports to the EU fell 24.4% in FY25, from $7.71B to $5.82B (GTRI), with steel alone crashing 35.1% to $3.05B - a decline that happened before CBAM duties even took effect. GTRI projects exporters may need to cut prices by 15-22% to retain EU buyers as the carbon levy moves from reporting to payment phase. Europe still absorbs roughly two-thirds of India's steel exports, meaning the bulk of the industry now needs verified carbon data fast.

Layer 4 - Carbon Market Access Platforms for Obligated Entities

- The opportunity: Carbon market access platforms - brokerage, analytics, and compliance management combined -that let India's industrial companies manage their carbon position in real time: track emission trajectory, model surplus or deficit, decide when to buy or sell, execute on the exchange. This is the Bloomberg terminal for Indian carbon, a product that doesn't exist yet and will be needed urgently once CCC trading opens. The voluntary market needs parallel infrastructure: buyer-seller matching, credit quality verification, price discovery, and portfolio management for corporates making net-zero commitments.

- The numbers: Around 490 entities already carry binding emission intensity targets under CCTS, rising to roughly 740 once all nine energy-intensive sectors are notified - most with no prior experience in carbon markets, pricing, or trading infrastructure. The Power Minister has indicated first CCC trades will launch by October 2026, giving these entities a narrow runway to build a trading capability from scratch.

Layer 5 - Transition Finance Platforms for Hard-to-Abate Sectors

- The opportunity: Platforms that structure, package, and match transition finance to specific industrial decarbonisation projects - green project bonds, blended finance structures, green loan origination platforms, and transition finance advisory tools.

- The Ecosperity panel on "The Transition Dilemma: Short-Term Returns vs Long-Term Decarbonisation" was, at its core, about this gap, and it remains largely unfilled by the startup ecosystem. Decarbonising steel, cement, and aluminium isn't a software problem; it's a capital allocation problem.

- The numbers: India needs $467 billion in climate finance by 2030 across its four most carbon-intensive sectors, with steel and cement alone accounting for over 80% of that total. The government has committed Rs 20,000 crore over five years to CCUS in Budget 2026-27, targeting power, steel, cement, refineries, and chemicals - but private capital at the individual project level remains thin.

Our Framing : Compliance is the new PMF

In Part 1, we argued that the grid doesn't need to be rebuilt - it needs to be made intelligent. The same logic applies to India's carbon market: it doesn't need a new policy framework. It has one. What it needs is the software, data, and financial infrastructure to actually run.

At Bluegreen, we believe compliance-driven markets create some of the clearest early-stage investment signals. When the government creates a legal obligation backed by financial penalties - as the CCTS does - it creates a buyer with urgency, a clear use case, and no optionality on timing. The carbon market equivalent of GST filing software is going to be built soon. The question is who builds it.

If you are building in the carbon market infrastructure space - reach out. We are paying attention.

In Part 1, we argued that the grid doesn't need to be rebuilt - it needs to be made intelligent. The same logic applies to India's carbon market: it doesn't need a new policy framework. It has one. What it needs is the software, data, and financial infrastructure to actually run.

At Bluegreen, we believe compliance-driven markets create some of the clearest early-stage investment signals. When the government creates a legal obligation backed by financial penalties - as the CCTS does - it creates a buyer with urgency, a clear use case, and no optionality on timing. The carbon market equivalent of GST filing software is going to be built soon. The question is who builds it.

If you are building in the carbon market infrastructure space - reach out. We are paying attention.