Why Emerging Venture Capital Managers Outperform Established Ones

Across global venture capital markets, a consistent empirical pattern has emerged that is usually never spoken about : emerging ( incl spin-out ) venture capital managers generate disproportionately higher upsides than established, large-scale GPs.

Global data suggests that while established funds tend to deliver more predictable, beta-like returns, emerging managers dominate the right tail of the return distribution, where venture capital actually creates value. This isn't a matter of opinion or narrative framing; it's a pattern that holds across institutional datasets : PitchBook, Preqin, Cambridge Associates, Carta, and StepStone datasets confirm it.

So, at BlueGreen, we decided to synthesize global evidence with India-specific case studies to answer four questions :

- Why Small funds are mostly Emerging managers / First time Funds ?

- Do Small Funds - First time Funds deliver higher IRRs ?

- Why scaling beyond Fund IV kills alpha, and why the Power law rewards the Small Funds ?

- What this means for LPs investing in Indian VCs

- Why Small funds are mostly Emerging managers / First time Funds ?

- Do Small Funds - First time Funds deliver higher IRRs ?

- Why scaling beyond Fund IV kills alpha, and why the Power law rewards the Small Funds ?

- What this means for LPs investing in Indian VCs

Let’s dive right in

A. Capital Concentration vs Alpha Generation

India's venture ecosystem has scaled rapidly over the last decade, producing a deep pipeline of high-growth startups and global-scale outcomes.

At the same time, venture fundraising, especially from institutions, has become increasingly concentrated among a small number of large, established platforms, a trend mirrored globally as LPs gravitate towards brand familiarity during periods of constrained liquidity. Ironically, many of these liquidity constraints originate from established managers themselves

However, we tend to forget that venture capital defies mean-reversion logic.

Venture returns follow a power-law distribution, where a small number of funds and an even smaller number of companies account for the majority of value creation. In such a system, minimising variance cannot be the primary objective; instead, accessing extreme positive outliers should be the goal when choosing the right GP, isn’t it ?

Who are these extreme outliers ?

B. Are Small Funds Mostly Emerging Managers and Not Established Ones ?

Before comparing performance, it is critical to establish a foundational point: small venture funds are overwhelmingly managed by emerging or early-vintage GPs, not by mature, established franchises.

This is not anecdotal; it is factual.

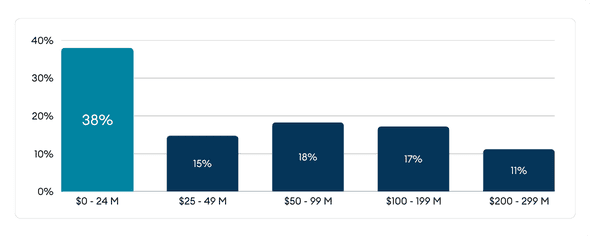

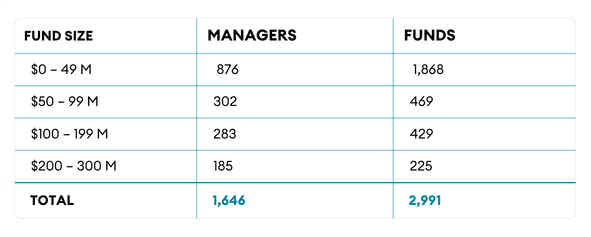

StepStone's analysis (cited by Chronograph) reveals that since 2018 over 3,000 US-based VC funds have been raised, with fund sizes below $300 Mn.

38% of these funds were under $25 Mn. 53% were under $50 Mn.

Critically, few managers maintain small fund sizes once they reach Fund IV or later.

Once a GP becomes established, capital scale almost always increases, because larger funds become easier to raise - “ No one got fired for hiring an IBM” kicks in as larger LPs like Fund of Funds or even sovereign Funds, gravitate towards brands that are familiar. It feels “safer”.

Established GPs have little incentive to shrink as well when they can garner more fees and expand their teams with “Titular Partners” to satisfy that team question if asked.

This leads to a clear analytical conclusion :

- Small venture funds are, mostly, early-vintage or first-time funds.

- Small venture funds are, mostly, early-vintage or first-time funds.

Thus, if small funds were to outperform, it is effectively emerging managers who are outperforming, not the large ones

Let's see in Part 2 whether small funds and first-time funds actually outperform the larger ones. Stay tuned.

Part 2

We continue with the series we started last week. We asked around and most felt it was something they had no idea about. In fact, they held beliefs to the contrary

Lets recount - In Part 1 of the series we examined :

The divergence between capital concentration in Established Managers and the power-law nature of venture returns around few companies that deliver most of the returns in a certain Vintage

How Small Funds are mostly, Emerging Managers and not Established Managers

The divergence between capital concentration in Established Managers and the power-law nature of venture returns around few companies that deliver most of the returns in a certain Vintage

How Small Funds are mostly, Emerging Managers and not Established Managers

Part 2 - deals with the next logical question: Do Small Funds - Emerging Managers deliver higher IRRs ? The answer is Yes.

Small Funds- Emerging Managers Deliver Higher IRRs

Multiple independent institutional datasets confirm that first-time and early-vintage VC funds materially outperform established funds on IRR. All figures below are in USD.

- Preqin (2017) reports:

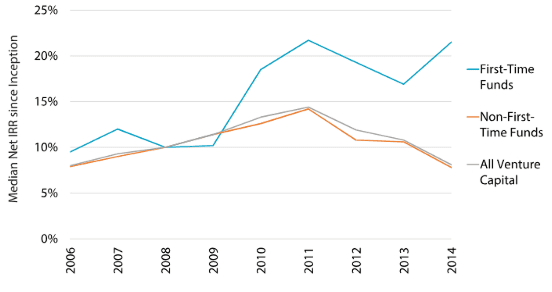

- Median net IRR for first-time VC funds(2006 – 2014 vintages): ~12.9%.

- Median net IRR forestablished VC funds: ~9.9%.

PitchBook (2019) finds (5):

First-time VC funds (2012–2014 vintages): 17.1% median IRR.

Follow-on funds raised by the same managers: 10.8% median IRR

- Median net IRR for first-time VC funds(2006 – 2014 vintages): ~12.9%.

- Median net IRR forestablished VC funds: ~9.9%.

PitchBook (2019) finds (5):

First-time VC funds (2012–2014 vintages): 17.1% median IRR.

Follow-on funds raised by the same managers: 10.8% median IRR

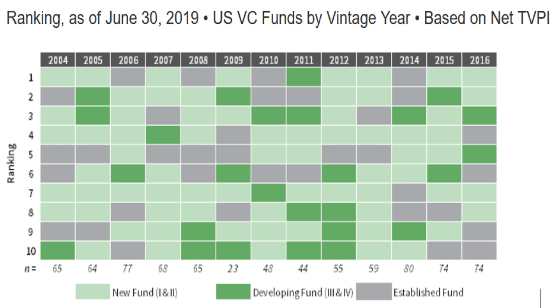

Cambridge Associates documents:

- New and developing venture funds (Funds I – IV) consistently account for

a large share of top-performing funds across vintage years. - Established managersappear less frequently among the highest-performing funds.

Cambridge Associates documents:

- New and developing venture funds (Funds I – IV) consistently account for

a large share of top-performing funds across vintage years. - Established managersappear less frequently among the highest-performing funds.

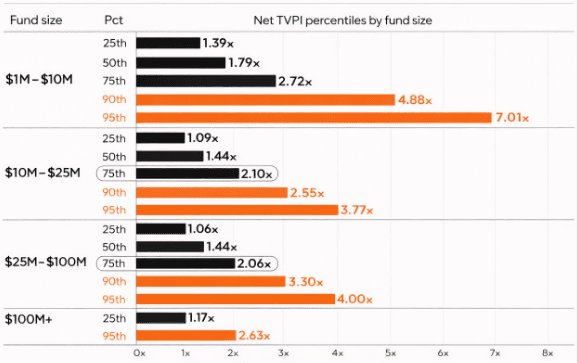

Carta Fund Admin Analysis (234 US Venture Funds) finds:

- Performance advantage is strongest when managers are early in the fund lifecycle, and this is consistent across vintages and market cycles

- Smaller funds (<$25M and <$100M) demonstrate stronger top-decile and top-quartile outcomes relative to larger funds (over $100M).

- Median returns are closer across size buckets, but right-tail dispersion favours smaller vehicles.

Carta Fund Admin Analysis (234 US Venture Funds) finds:

- Performance advantage is strongest when managers are early in the fund lifecycle, and this is consistent across vintages and market cycles

- Smaller funds (<$25M and <$100M) demonstrate stronger top-decile and top-quartile outcomes relative to larger funds (over $100M).

- Median returns are closer across size buckets, but right-tail dispersion favours smaller vehicles.

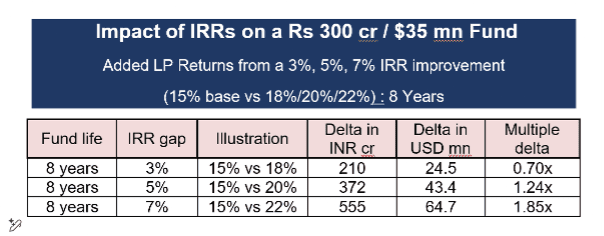

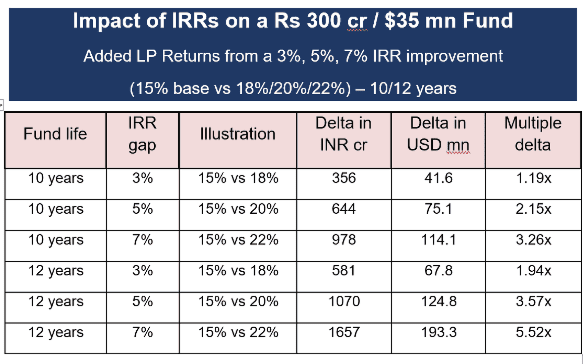

B. The Impact of Outperformance Over 8/10/12yrs

Seemingly small - Single digit differences in IRRs between Emerging Managers vs Established Managers may appear modest at first glance.

However, for LPs, the implications over a full fund lifecycle are far from incremental. Even small variances in IRR compound meaningfully over 8–12 year holding periods, translating into significant differences in total value created.

To illustrate this, we present a simple visualisation below :

Thus, in a power-law asset class, differences between top-quartile and median performance may appear small in IRR % terms, but translate into dramatically different outcomes over time.

For family offices, HNIs and institutional allocators,this raises an important question : are current portfolios positioned to access these outliers basis a Top quartile Track Record - or primarily allocated to familiarity and perceived safety ?

So, at the end of Part 1 and 2, we have the following conclusionse end of Part 1 and 2, we have the following conclusions :

- There is a divergence between capital concentration in Established Managers and the Power-law nature of venture returns

- How Small Funds are mostly Emerging Managers and not Established Managers

- Small Funds - Emerging Managers Outperform Larger Established Managers resulting in outsized returns to LP

- There is a divergence between capital concentration in Established Managers and the Power-law nature of venture returns

- How Small Funds are mostly Emerging Managers and not Established Managers

- Small Funds - Emerging Managers Outperform Larger Established Managers resulting in outsized returns to LP

But outperformance data alone tells only half the story. The next edition, Part 3, explores the deeper question:

Why do Small Funds deliver better performance vs Established Funds and and why does it evaporate as funds scale?

Part 3

Let’s recount. In Part 1 and Part 2, we established:

Let’s recount. In Part 1 and Part 2, we established:

Venture capital is a power-law asset class

Capital is concentrated in Established Managers (>Fund IV)

Small funds are overwhelmingly Emerging Managers

Emerging Managers consistently deliver higher IRRs

Venture capital is a power-law asset class

Capital is concentrated in Established Managers (>Fund IV)

Small funds are overwhelmingly Emerging Managers

Emerging Managers consistently deliver higher IRRs

This leads to the deeper question:

This leads to the deeper question:

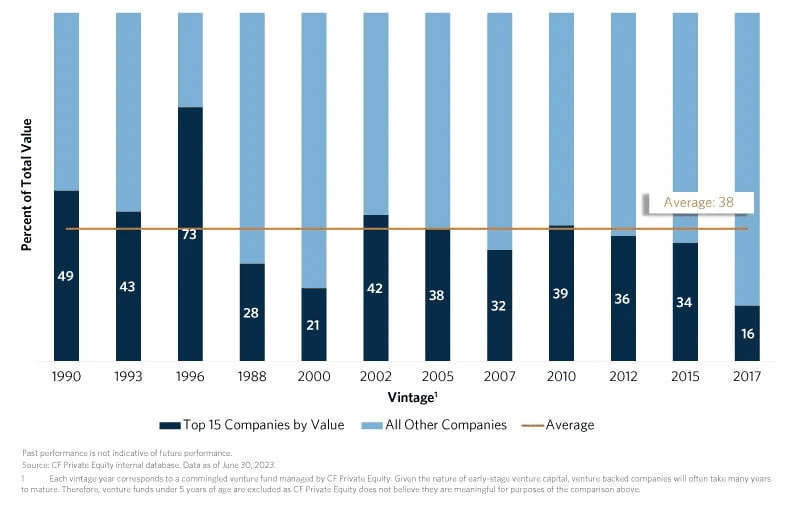

Venture Returns Are Driven by Outliers

- Venture outcomes are not evenly distributed.

- Across decades of US and European data published by The VC Factory 👍:

- A small number of companies drive a disproportionate share of returns per vintage

- Often, ~1–2% of capital generates >50% of portfolio value

- Vintage = Year of first Close of Funds paired together for benchmarking returns. (Source: The VC Factory, Commonfund)

- This is the structural reality of the asset class. Which leads to an important implication:

- ✳️ Access to outliers -not diversification- drives performance

- A small number of companies drive a disproportionate share of returns per vintage

- Often, ~1–2% of capital generates >50% of portfolio value

Who Captures These Outliers?

- If outliers drive returns, then the question becomes:

- ✳️ Which funds actually capture them?

- Global data (and early India evidence) suggests:

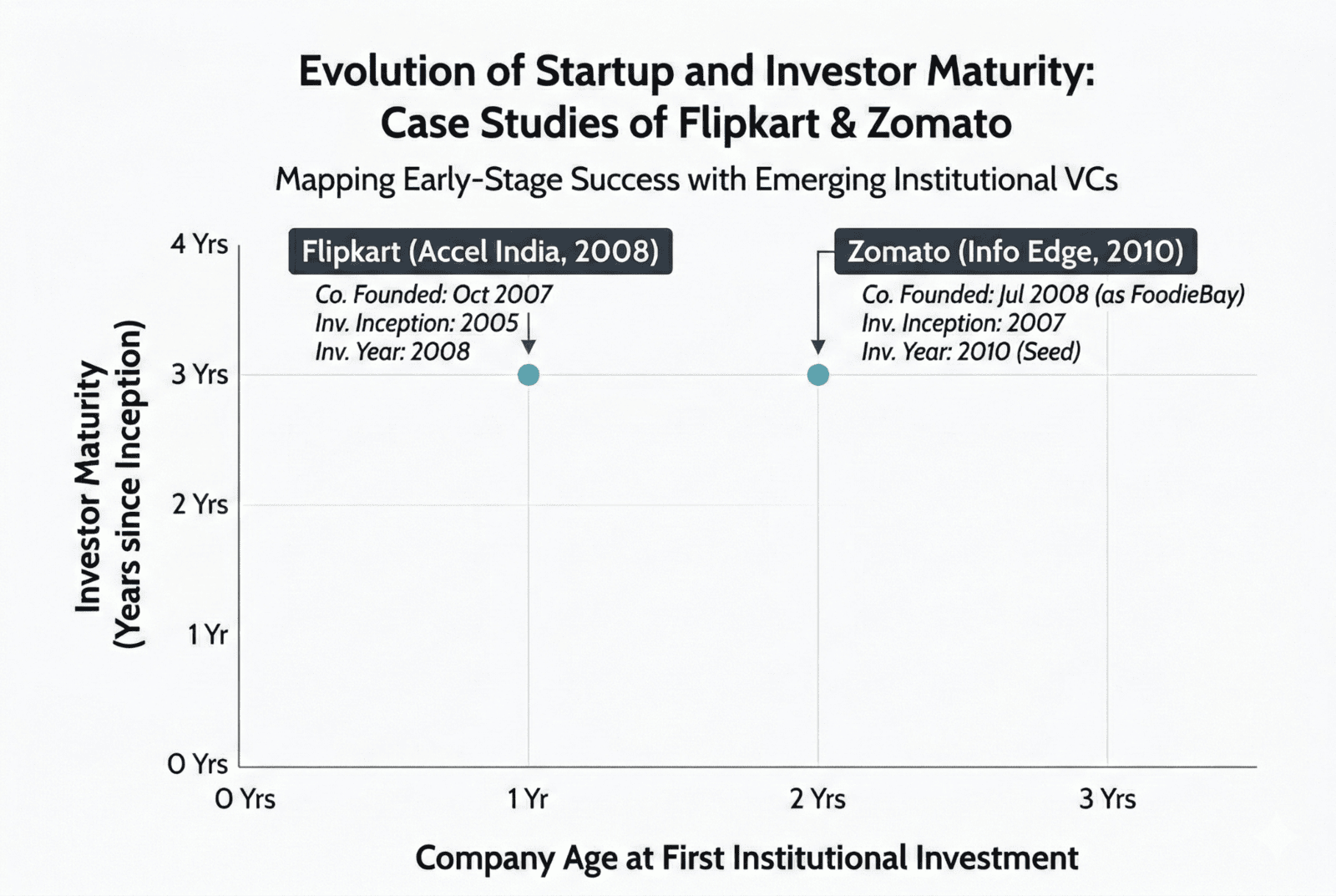

- These outliers are typically backed early by small, emerging managers.

- For example in India:

- Flipkart: backed early before institutional capital scaled

- Zomato: early backing preceded capital scale

- In both cases: Value creation began before capital scale arrived.

- ✳️ Which funds actually capture them?

- These outliers are typically backed early by small, emerging managers.

- Flipkart: backed early before institutional capital scaled

- Zomato: early backing preceded capital scale

What Changes When Funds Scale?

If emerging managers outperform, why does this advantage decline over time?

Because scaling a fund changes its structure.

Fund Size Expansion

Larger pools of capital require broader deployment, reducing the ability to:

a) Concentrate capital

b) Back a small number of high-conviction ideas

Strategy Migration:

As funds grow:

a) Early-stage investors move to later-stage investing

b) Entry valuations increase c) Ownership levels decline

The result: Lower return multiples.

Deployment Pressure

Larger funds must deploy more capital within fixed timeframes. This often leads to:

a) Faster decision cycles

b) Inclusion of marginal opportunities

Ownership Dilution

Competitive rounds and larger cheque sizes reduce ownership. In venture: Ownership drives outcomes.

Partnership and Incentive Drift

The most under-discussed risk in venture capital isn’t market risk. It’s team drift. Over time, inside many firms:

a) The partners who drove early outperformance ie Rainmakers, often exit

b) Decision-making shifts from conviction-led individuals to consensus-led committees

c) Economic incentives fragment across the partnership

Nothing looks broken on the surface. The brand remains. The track record remains. The narrative remains.

But something important has changed. Over time, this disconnect compounds.

And it creates a subtle but critical gap: You think you are backing a proven track record and an old firm But you are actually underwriting a new team.

In a power-law asset class, that gap is not incremental. It is decisive

Fund Size Expansion

Larger pools of capital require broader deployment, reducing the ability to:

a) Concentrate capital

b) Back a small number of high-conviction ideasStrategy Migration:

As funds grow:

a) Early-stage investors move to later-stage investing

b) Entry valuations increase c) Ownership levels decline

The result: Lower return multiples.Deployment Pressure

Larger funds must deploy more capital within fixed timeframes. This often leads to:

a) Faster decision cycles

b) Inclusion of marginal opportunitiesOwnership Dilution

Competitive rounds and larger cheque sizes reduce ownership. In venture: Ownership drives outcomes.Partnership and Incentive Drift

The most under-discussed risk in venture capital isn’t market risk. It’s team drift. Over time, inside many firms:

a) The partners who drove early outperformance ie Rainmakers, often exit

b) Decision-making shifts from conviction-led individuals to consensus-led committees

c) Economic incentives fragment across the partnership

Nothing looks broken on the surface. The brand remains. The track record remains. The narrative remains.

But something important has changed. Over time, this disconnect compounds.

And it creates a subtle but critical gap: You think you are backing a proven track record and an old firm But you are actually underwriting a new team.

In a power-law asset class, that gap is not incremental. It is decisive

Why Emerging Managers Are Structurally Different

Emerging managers are not smaller versions of established funds :

- Smaller fund sizes force high-conviction investing

- Early-stage focus enables higher ownership and multiples

- Partners remain closer to decisions and outcomes

- Incentives are tightly aligned with LP outcomes

- Smaller fund sizes force high-conviction investing

- Early-stage focus enables higher ownership and multiples

- Partners remain closer to decisions and outcomes

- Incentives are tightly aligned with LP outcomes

In a power-law asset class: This alignment is the edge. They are structurally aligned with how venture capital actually creates value.

What Comes Next

In venture, we have shown how a few companies drive most returns.

What is less understood is that a small number of funds - and even fewer individuals -consistently capture them.

For LPs, this shifts the problem: From selecting funds to identifying who within them actually creates outliers

✳️ How do you find these repeat “Rainmakers”?

That is what we explore in Part 4.

Part 4

Its time for us to conclude the Series with some clear actionables that can make the difference between average to below benchmark returns to outlier returns.

To remind, this series began with analysis of global data from over 1700 Funds and leading independent benchmarking firms

In Parts 1-3, we established a structural contradiction :

Venture capital is a power-law asset class

Most returns per Vintage are concentrated in a small number of outlier companies

Capital is concentrated in Established Managers (> Fund IV)

Even though, Emerging Managers consistently outperform Established ones

A small number of individuals consistently identify and back these outliers - These are the Rainmakers

As funds scale > Fund IV and become larger & Established , structural dilution accompanied by the exit of key Rainmakers - erodes returns

Venture capital is a power-law asset class

Most returns per Vintage are concentrated in a small number of outlier companies

Capital is concentrated in Established Managers (> Fund IV)

Even though, Emerging Managers consistently outperform Established ones

A small number of individuals consistently identify and back these outliers - These are the Rainmakers

As funds scale > Fund IV and become larger & Established , structural dilution accompanied by the exit of key Rainmakers - erodes returns

This shifts the problem for LPs: From Funds to Individuals

From selecting funds to identifying the individuals behind these outliers

The Source of the Mismatch

If returns are driven by individuals, why does capital concentrate at the firm level?

Because:

Track record is presented at thefirm level

While outcomes are created at theindividual level

Over time, this creates a disconnect: Capital follows brands. Returns follow decision-makers

Implication for LPs

In many cases, by choosing such Funds where Rainmakers have left, LPs are effectively: backing a historical track record with a different set of decision-makers

Same Established VC firm.

Different people today.

Yet the same track record continues to be presented

The Implication:

if returns are driven by a few individuals, and those individuals are no longer in the firm,

✳️ What exactly is an LP underwriting?

In a power-law asset class, that gap is not incremental.

It is decisive. Brand Logos don’t drive returns. Individuals who lead investments do.

How to close the missing Layer : Attribution Check

This is where most diligence stops. LPs evaluate:

- Portfolio construction

- Vintage returns

- Firm-level performance

- Portfolio construction

- Vintage returns

- Firm-level performance

✳️ But rarely: Who actually created those outcomes?

To bridge this gap, Investors need to move from: portfolio-level evaluation → deal-level attribution

We refer to this as the #AttributionCheck

Step 1: Identify Investment Leads

For each portfolio company: ✳️ Who was the Investment Lead?

The individual who:

- Originated the deal - Check the IC Note

- Issued the first term sheet

- Owned the investment decision

Classify them as:

- Founding Partner ( A )

- Rainmakers, Now Exited Partners (B, C )

- New Partners ( D, E etc)

- Originated the deal - Check the IC Note

- Issued the first term sheet

- Owned the investment decision

- Founding Partner ( A )

- Rainmakers, Now Exited Partners (B, C )

- New Partners ( D, E etc)

Step 2: Independently Verify

Do not rely solely on GP disclosures. Cross-check through:

- Founder conversations

- Public announcements and in PitchBook, Preqin databases

- Founder conversations

- Public announcements and in PitchBook, Preqin databases

Any inconsistency is a red flag

Step 3: Map Value Creation

For the active portfolio:

✳️ What proportion of outcomes were led by current vs former Investment Leads?

This revealswhere returns actually originated

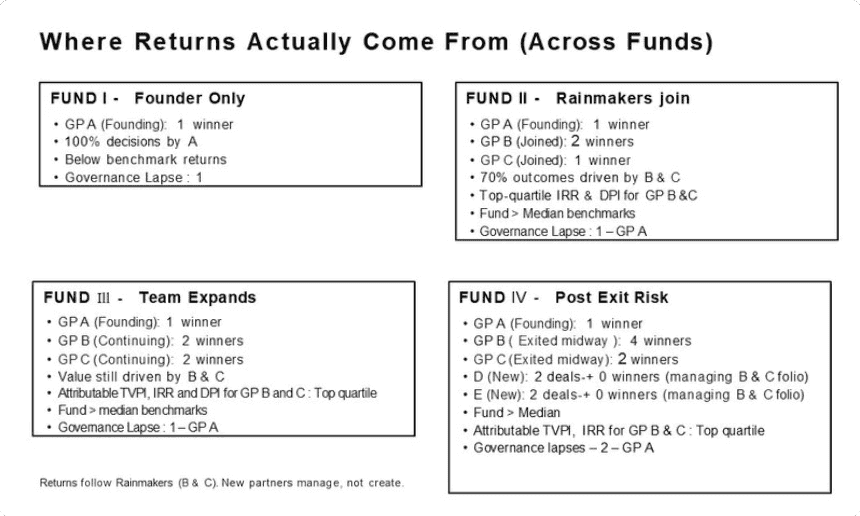

Sample chart :

This is where most diligence stops. LPs evaluate:

- Portfolio construction

- Vintage returns

- Firm-level performance

- Portfolio construction

- Vintage returns

- Firm-level performance

Step 4: Assess Continuity Risk

If a significant share of outcomes were created by individuals who have exited:

✳️ The current team is managing outcomes they did not originate

This represents a material underwriting risk

👉 Founder alone → underperforms benchmarks

👉 Rainmakers join → outperformance

👉 Rainmakers exit → performance risk returns

Step 5: Compare Performance by Individual

Evaluate: ✳️ Outcomes generated by past vs current Investment Leads

If: Past > Current, it raises questions on:

- Team quality

- Incentive structures

- Retention of top performers

- Team quality

- Incentive structures

- Retention of top performers

Step 6: Examine Incentives and Stability

Look for patterns:

- Senior team churn

- Disproportionate carry allocation

- Exit of Rainmakers- reach out and conduct exit interviews

- Senior team churn

- Disproportionate carry allocation

- Exit of Rainmakers- reach out and conduct exit interviews

In VC, alignment and longevity matter

Step 7: Attribute Losses

Not just wins. Evaluate:

✳️ Who led investments that were written off?

✳️ Who had governance lapses in their investments ? A repeated pattern across Funds ?

✳️ Was more Capital given to Founding Partner-led companies even though most Returns were driven by Exited Rainmakers ?

Patterns in losses are often as revealing as successes.

See Sample chart again

What This Reveals

In venture:

- A few companies drive returns

- A few funds capture them

- A few individuals create them

- A few companies drive returns

- A few funds capture them

- A few individuals create them